We believe that every family deserves the opportunity to own their own home, and our partnership with EastWest Bank brings us one step closer to ...

Read More >

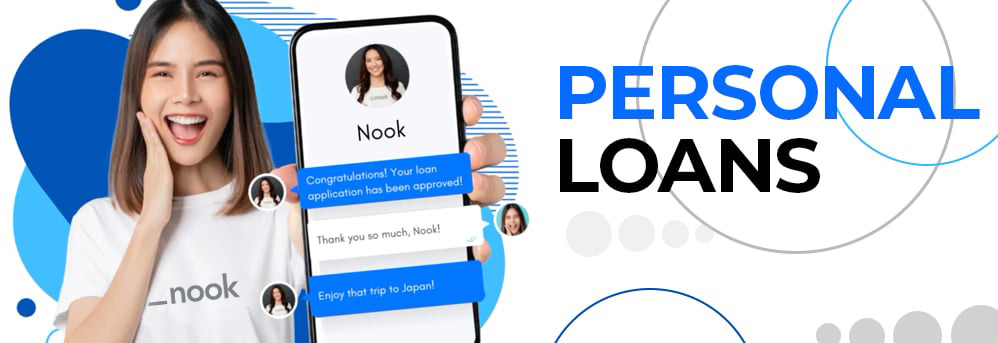

![]() 6,000+ people started their loan in the last 30 days

6,000+ people started their loan in the last 30 days

![]() 6,000+ people started their loan in the last 30 days

6,000+ people started their loan in the last 30 days

Great concept and service from Nook. A big help to clients seeking home loans in the Philippines.

Jose P.

You guys are super Good! I am very happy that Nook is now available here in the Philippines.

Marra D

If there's 11, I'll go with 11 rating! I recommended Nook to my colleagues and friends.

Angelie T

Super Good Service from Nook! Your company is a big help to us Filipino's abroad.

Warlyn P

I didn't expected that my home loan would be approved this fast. All perfect for me!

Joseph and Axel S

You guys have a good service. I'm always updated with my application with RCBC.

Flor M